Quantitative Consulting

Eliminating conjecture through algorithmic validation and institutional-grade risk modeling.

Forensic Backtest Engineering: Moving beyond "in-sample" bias via Walk-Forward Validation and Synthetic Data Overlays to isolate non-random statistical edges.

Rigorous Logic | Systematic Execution

In a market saturated with 'narrative-driven' strategies, we provide the mathematical bedrock. Our quantitative consulting services are designed for fund managers, professional traders, and family offices who require absolute certainty in their execution logic. We don't just build models; we stress-test them against a decade of market regimes to ensure they are built to survive, not just to perform.

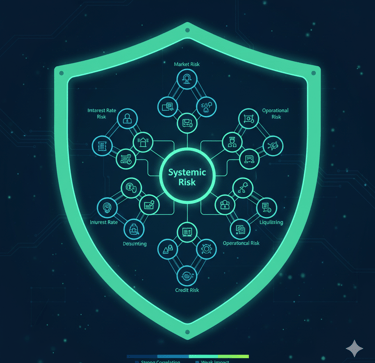

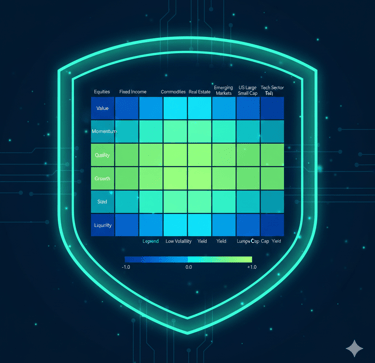

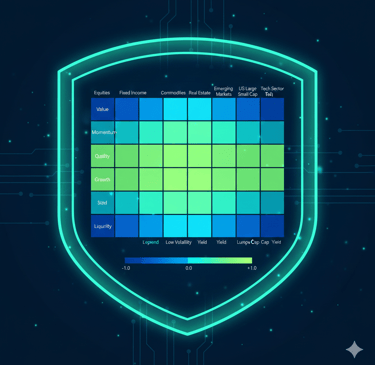

High-Dimensional Portfolio Construction: Utilizing Mean-Variance Optimization and Risk-Parity Frameworks to architect portfolios that are resilient to regime-specific volatility.

Ex-Ante Risk Factor Attribution: Decomposing expected returns to ensure diversification is truly structural, not just nominal.

Systematic Execution Architecture: Engineered connectivity within the Interactive Brokers (IBKR) ecosystem, utilizing Python-driven API wrappers to eliminate discretionary decisions.

Case Study: Systematic Execution Framework

A hedge fund sought to transition from manual trading to a high-fidelity automated system for stocks and options. The objective was to eliminate emotional decision-making by automating the lifecycle of long and short positions through quantitative rules.

The Solution: The Four-Pillar Architecture

The firm implemented a modular system designed for Interactive Brokers (IBKR) integration:

Data & Quant Engines: Processes real-time feeds to calculate proprietary metrics at specific intraday intervals.

Trading Rules Engine: Automatically calibrates position sizes based on current Total Portfolio Value.

Hybrid User Interface: Features a "one-click" execution for manual trades and a "two-minute pause" for automated triggers to ensure human oversight before final routing.

The Strategy: Quantitative Guardrails

The system utilizes rigorous "Buy Signal" logic to identify high-probability entries: Technical Thresholds, Fundamental Filters and Risk Calibration.

The Results: Disciplined Alpha

Automated Risk Management: Implemented hard-coded "Take Profit" and "Stop Loss" exits.

Operational Control: An "Emergency Stop" feature allows for immediate cessation of all automated activity during extreme market volatility.

Precision Execution: Orders are routed as buy limits at the bid-ask midpoint to minimize slippage.

Risk Disclosure & Forensic Limitations Investing in financial instruments involves substantial risk, including the possible loss of principal. Quantitative strategies, backtested results, and algorithmic models are based on historical simulations and are not guarantees of future performance. Market conditions can change rapidly, and technical factors such as API connectivity, software latency, or execution errors may impact realized results. Furthermore, Founders Vetting and due diligence reports are forensic assessments based on point-in-time data and behavioral analysis; they are designed to identify narrative and operational risks but do not eliminate the possibility of underlying fraud, business failure, or future leadership volatility. MVK Alpha Capital does not provide guaranteed returns or capital preservation. All investment and deployment decisions—whether based on algorithmic signals or vetting audits—are made at the client's sole discretion and risk.